NFTs – a useful technology or a wasteful scam?

")

Non-fungible tokens, commonly called NFTs, have become the topic of controversy lately. Being uniquely identifiable units of data stored on a cryptographic blockchain, NFTs have gained use as a way to trade artwork and other virtual items. The main controversy surrounding NFTs tends to focus on the significant energy cost of transactions on a blockchain, the lack of any legal recognition of ownership represented by an NFT, and the high amount of scams associated with NFTs. This article explores various pros and cons of non-fungible tokens.

What are NFTs?

In order to understand NFTs, one must first understand cryptocurrency. Cryptocurrency is digital money: you can’t touch it, but you can still own, give, and receive quantities of it. The difference between cryptocurrency and, say, your PayPal balance is that most cryptocurrencies are not governed by any central authority. They’re decentralized — there is no company that “owns” Bitcoin, for example.

The principle of decentralized cryptocurrencies lies in a data structure called a blockchain serving as a transaction ledger. Without going into too much detail, there are three main things to understand about the cryptography behind these currencies. One is that a copy of the blockchain is held on every node, which is a computer that is part of the cryptocurrency network. Two is that the blockchain is write-only — you can add something to it, but you can’t delete information from it. And three is that, for most cryptocurrencies, the process of verifying new transactions is very energy-intensive, utilizing a consensus mechanism known as proof-of-work that involves several computers trying to solve a purposely difficult computational problem. This video by 3Blue1Brown on YouTube explains the concept well.

So, where do NFTs come into the mix? Well, some cryptocurrency blockchains support tokens other than the original cryptocurrency. For example, the Ethereum blockchain keeps track of transactions for the Ethereum currency itself as well as other tokens like Tether, USDCoin, etc. A fungible token is one that isn’t unique in itself: the cryptocurrencies themselves are examples of fungible tokens. It then follows that a non-fungible token, aka NFT, is unique: you can think of a fungible token as being a dollar bill, and a non-fungible token as being a painting. Both the dollar bill and the painting have value and can be traded, but the difference is that there are millions of other dollar bills but only one of that painting. On the blockchain, both the dollar bill (cryptocurrency), and the painting (NFT) get assigned ownership to a wallet — and, just like with cryptocurrency, an NFT can be sent to and received from other wallets on the network. An NFT typically has both a unique ID as well as a piece of data stored differentiating it from other tokens on the network.

NFTs as digital art

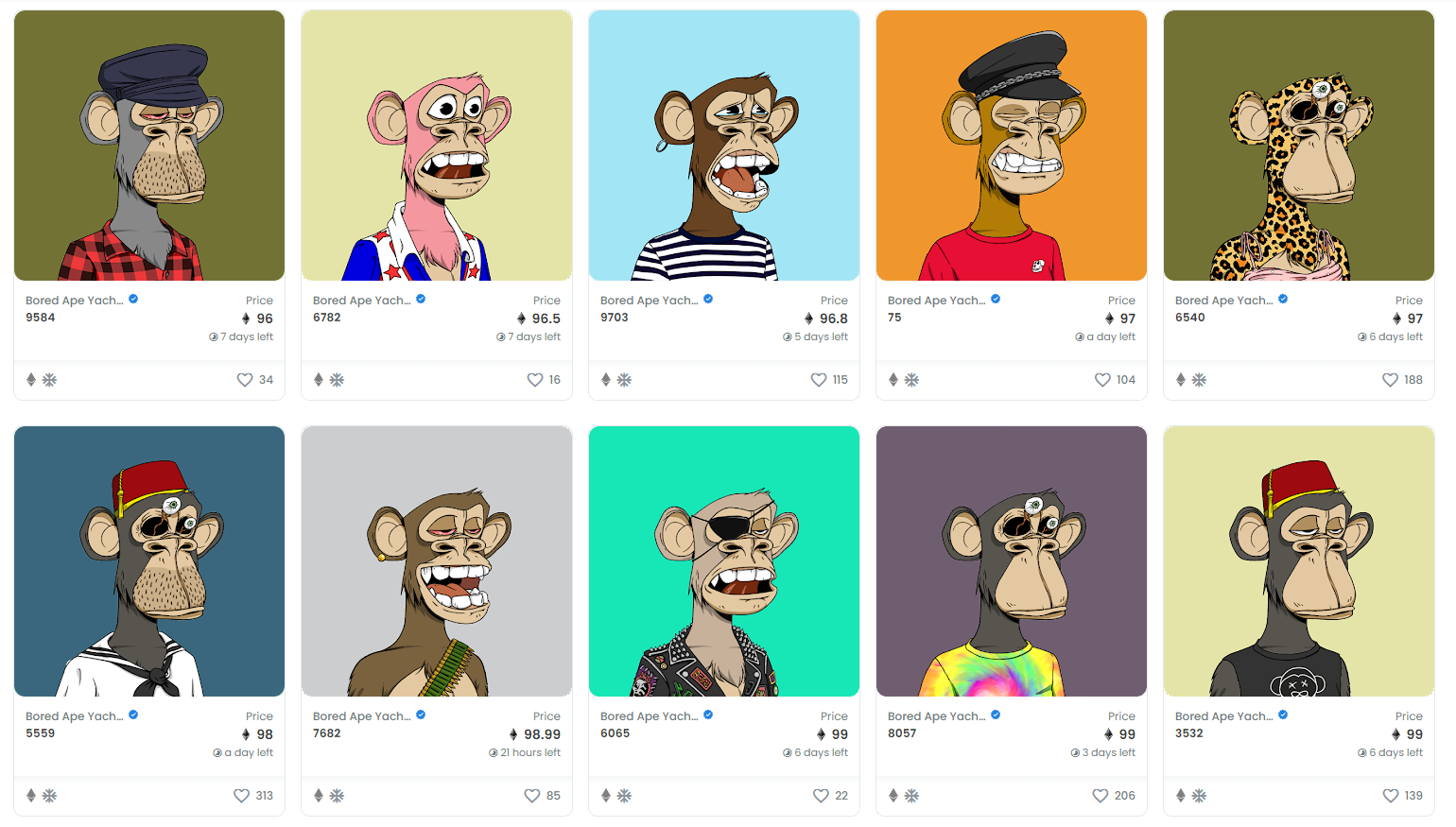

Speaking of paintings, one of the most popular use cases for NFTs has been for the sale of digital art. An artist can “mint” their artwork as an NFT, and sell or auction it off online, with the potential buyer getting to “own” the art piece on the blockchain. Online marketplaces like OpenSea and Rarible have gained tremendous popularity recently, with thousands of digital art pieces being sold for thousands, or even millions of dollars worth of Ethereum. The images sold tend to be part of collections of thousands of other similar, but different, images. Some examples are collections like the Bored Ape Yacht Club, and CryptoPunks, images from which retail for hundreds or even thousands of ETH. At the time of writing this, 1 ETH is worth about three thousand dollars. For comparison, Banksy’s “Girl With Balloon” real-life artwork was auctioned off for 1.4 million in 2018, before the art famously shredded itself. Point is, the amount of money flowing through this digital art market is no joke.

“Bored Ape Yacht Club” NFTs are selling for over $200,000 worth of Ethereum on OpenSea. Who would have thought people would pay this much for a digital image of a cartoon monkey?

NFTs in games

Another use case for NFTs has been to represent digital items owned by one’s avatar in virtual worlds, which some have recently started calling “metaverses”. For a game developer wishing to make in-game items tradable for real-world money, building their platform on top of NFTs and cryptocurrency can be preferable to setting up payment processing for real money, as there tend to be less regulatory laws governing the use of cryptocurrency.

The pandemic has seen a rise in the popularity of “play-to-earn” online games: games where the virtual currency and items you earn can be exchanged for real-world money. One such example is Axie Infinity, an online game where your playable character is an NFT and the in-game currency can be directly exchanged for cryptocurrency and real money. The game has become very popular in the Philippines and other developing countries, where the pandemic has caused many to lose their jobs. Another example is Decentraland, a virtual social world where one can buy and sell virtual property using cryptocurrency. These games, however, have a catch: in order to make money, you have to spend money. In the case of Axie Infinity, the cost to buy the player character needed to play the game has been steadily rising — as of right now, the cost to buy a basic “team” is a little over one hundred USD.

The Cons

At the beginning of this article, I said we would explore both the pros and cons of NFTs. Unfortunately, it is difficult to name any “pros” past the usefulness of the technology itself, which is a matter of debate at best. As for the cons, however, many can be named.

NFTs carry no ownership

NFTs are commonly used to represent digital art: where in real life you would buy a painting, you would buy an NFT in the digital world. However, buying an NFT of an image does not actually give you any rights to use the image represented by the NFT. You don’t even get the image itself attributed to you on the blockchain: image file sizes are typically too big to make storing them on a blockchain practical. Instead, a link to the image is attributed to you. So, buying an NFT is essentially just buying a hyperlink — you get no legal rights to use the image the link points to, nor do you have any control over what the link points to. If the image gets deleted from the server storing the file, your NFT will become a useless, broken link (not that it was very useful to begin with). In essence, NFTs are just receipts, “certificates of ownership” if you will.

Energy Use

As mentioned before, in order to verify transactions, most cryptocurrencies are reliant on a network of miners spending time and energy solving a cryptographic problem, with the spent resources essentially “vouching” for the transaction in a mechanism known as proof-of-work. The most popular platform for NFTs as of right now is the Ethereum blockchain, which uses proof-of-work — meaning tremendous amounts of energy are used in order to verify each transaction on the network. Currently, the amount of energy spent to verify an Ethereum transaction is a little over 230 kilowatt-hours. To put this number into perspective, the average monthly household electricity consumption for an American household in 2020 was 893 kWh. Yes, that’s right — a single Ethereum transaction uses a week’s worth of your typical electricity bill. Given the current global energy crisis, using such enormous amounts of electricity to support a digital market of cartoon monkey images is incredibly wasteful.

Scams

Due to the lack of regulation combined with the lack of public knowledge on the subject, the world of cryptocurrency and NFTs is filled with scams on every corner. Anyone wishing to enter the market should be wary of the thousands of phishing sites posing as legitimate NFT marketplaces. And as for the “legitimate” marketplaces themselves, the entire NFT market can be described as being a Ponzi scheme — a form of investment fraud that pays existing investors with funds collected from new investors. In other words, if you buy an NFT with hopes of selling it for a higher price later, you’re reliant on a future “investor” valuing the imaginary asset more than you do. Calling such a practice “investing” is a misnomer — it’s gambling, or speculation at best.

The Verdict

So, are NFTs a useful technology, or are they a wasteful scam? Well, considering the fact that they’re essentially digital certificates of ownership with no legal basis that are built on an incredibly energy-inefficient system that have many scams associated with them and are even called scams themselves, I’d say it is definitely the latter.